INSIGHT

Build-to-Rent and the Future of Housing in United Kingdom:

Structural Supply Constraints, Institutional Capital, and the Growth of Rental Communities

By: Arman Rahimi, MSc

About the Author

Arman Rahimi is a property developer and a real-estate professional, specialising in residential development and large-scale housing projects in London. With experience across development management, project delivery and investment strategy, his work focuses on the evolving relationship between housing supply, urban development and institutional capital in the UK residential market.

www.linkedin.com/in/arman-rahimi-uk

Content Page

- Executive Summary 2

- Introduction 4

- Evolution of Britain’s Housing System 5

- Structural Constraints on Housing Supply 6

- The Erosion of the Homeownership Pathway 8

- Institutionalisation of Rental Housing 10

- Planning Complexity and Barriers 12

- The Future Role of Build-to-Rent 13

- Conclusion 15

For general readers: Build-to-Rent (BTR) refers to residential developments designed and constructed specifically for long-term rental occupancy rather than individual unit sales. In the United States, it is a more established model with many decades of history, known as (multifamily housing), but it is a relatively new form in the UK since 2010’s.

…

- Executive Summary

The main 3 forces behind BTR

Housing Supply Constraints

Build to Rent Institutional Capital

Rental Demand

Structural Forces Behind the Emergence of a New Housing Asset Class

The growth of Build-to-Rent reflects the convergence of housing scarcity, demographic change and the global search for long-term income assets

The United Kingdom’s housing system is undergoing a structural transformation. Persistent constraints on housing supply, declining access to homeownership and the growing presence of institutional capital are reshaping the way housing is delivered, financed and managed.

For much of the late twentieth century the British housing system rested on two principal pillars: owner-occupation and social housing. Over time, however, structural pressures have altered this balance. House prices have risen significantly relative to incomes, access to mortgage finance has tightened and demographic changes have increased demand for flexible forms of housing tenure. As a result, a growing share of the population now relies on rental housing for longer periods of their lives.

At the same time, institutional investors such as pension funds, insurance companies and global investment managers have increasingly sought stable long-term income-generating assets. Residential rental housing, when delivered and managed at scale, has emerged as a sector capable of meeting these investment requirements.

Within this context, Build-to-Rent (BTR) has developed as a new institutional asset class within the UK residential market. Unlike traditional private renting, which has historically been dominated by fragmented individual landlords, BTR developments are designed as professionally managed rental communities supported by long-term institutional capital.

This paper argues that the expansion of Build-to-Rent reflects the convergence of three structural forces shaping the UK housing system:

- persistent constraints on the supply of new housing

- long-term growth in demand for rental accommodation

- the increasing role of institutional capital in residential real estate

As these forces continue to evolve, Build-to-Rent is likely to become an increasingly important component of the UK housing landscape. While it will not replace existing housing tenures, it represents the emergence of a new institutional framework for delivering rental housing at scale.

Understanding the structural drivers behind this transformation is essential for policymakers, investors and developers seeking to navigate the future of the UK housing market.

Case Study

Large institutional investors have increasingly partnered with developers to deliver rental housing at scale. For example, developments such as the East Village neighbourhood in Stratford (originally built for the London 2012 Olympic Games) have since been transformed into a major Build-to-Rent community. The neighbourhood now contains thousands of professionally managed rental homes operated by institutional investors, demonstrating the viability of large-scale rental housing in the UK market.

- Introduction

Evolution of the UK Housing System

1900s 1945-1980 1980-2010 2010-Present

Renting → Social Housing → Homeownership → Institutional Rental

Britain’s housing debate has for decades centred on the same themes: affordability, planning reform, and the political aspiration to expand homeownership. Yet beneath these recurring debates a more fundamental transformation is taking place. The UK housing system itself is evolving. The long-standing model built around owner-occupation and state-provided housing is gradually giving way to a third pillar: professionally managed rental housing funded by institutional capital.

This emerging sector [commonly referred to as Build-to-Rent (BTR)] has grown rapidly over the past decade. Initially concentrated in major cities such as London and Manchester, BTR developments are now appearing across the country and are attracting increasing interest from pension funds, insurance companies and global investment managers seeking long-term income-generating assets. What was once a fragmented private rental market dominated by small individual landlords is beginning to evolve into a more professionalised and institutionalised form of housing provision.

The emergence of BTR is sometimes described as a cyclical response to temporary pressures in the housing market. However, such interpretations underestimate the depth of the structural forces shaping Britain’s housing economy. The growth of professionally managed rental housing reflects a convergence of long-term trends: persistent constraints on housing supply, the erosion of traditional pathways into homeownership, and the search by institutional investors for stable long-duration assets capable of generating predictable income.

This paper argues that Build-to-Rent is not merely a new product within the housing market but a manifestation of a deeper structural shift in how housing is financed, delivered and managed in the United Kingdom. Understanding the drivers behind this transformation is essential for policymakers, investors and developers alike.

To examine this transition, the paper explores three interrelated forces shaping the evolution of the UK housing system:

- structural constraints on the supply of new housing

- long-term demographic and economic drivers increasing demand for rental accommodation

- the growing role of institutional capital in residential real estate

Together these forces are reshaping the nature of housing provision in Britain and positioning Build-to-Rent as a significant component of the country’s future housing landscape.

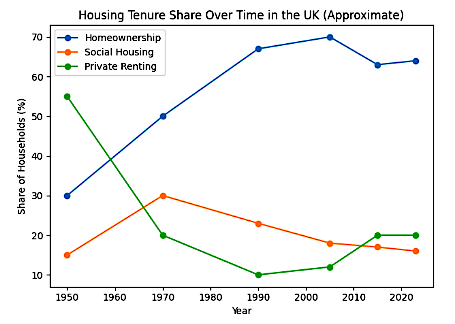

- Evolution of Britain’s Housing System

To understand the emergence of Build-to-Rent it is necessary to view it within the broader historical evolution of housing tenure in the United Kingdom. Britain has not always been a nation of homeowners. In fact, for much of the twentieth century the country was predominantly a nation of renters.

At the beginning of the twentieth century the vast majority of households lived in rented accommodation. Urbanisation during the industrial era had produced large concentrations of working-class housing in cities, often characterised by overcrowded conditions and limited sanitation. Addressing these conditions became a central concern of public policy in the aftermath of the First World War.

The government’s response was the introduction of large-scale public housing programmes designed to improve living standards for working families. The Housing and Town Planning Act of 1919, often associated with the “Homes for Heroes” programme, provided state support for local authorities to build new housing. Early council housing developments frequently drew on the principles of the Garden City movement, aiming to provide healthier living environments with access to green space and improved infrastructure.

Following the Second World War, the scale of public housing provision expanded dramatically. Wartime destruction, combined with longstanding housing shortages, led to extensive state-led construction programmes during the 1950s and 1960s. Local authorities became major providers of housing across the country, building large estates intended to accommodate growing urban populations. In many cases, these programmes represented ambitious social and political experiments aimed at improving living standards and reshaping urban environments.

For several decades Britain’s housing system therefore rested on two principal pillars: social housing delivered by the state and private homeownership. The balance between these tenures shifted significantly from the late twentieth century onwards, particularly following the introduction of policies encouraging the sale of council housing to tenants. Over time this transformation contributed to a decline in the stock of social housing and a growing reliance on private markets to meet housing demand.

The consequences of this shift continue to shape the housing landscape today. As social housing provision contracted and house prices increased relative to incomes, increasing numbers of households became reliant on the private rental sector. Yet the structure of that sector remained largely unchanged, dominated by small individual landlords and characterised by inconsistent quality of management and service provision.

Against this backdrop, the emergence of Build-to-Rent can be understood as part of a broader transition in the organisation of housing provision; one in which residential property increasingly resembles other institutional real estate asset classes such as offices, logistics and student accommodation.

Structural Constraints on Housing Supply in the United Kingdom

“UK governments have repeatedly stated the need to deliver approximately 300,000 homes per year in England in order to address long-term housing shortages.” Source: UK Government housing policy statements

A central factor shaping the evolution of Britain’s housing system is the persistent constraint on the supply of new homes. Estimates suggest that the United Kingdom faces a structural housing shortage of between three and four million homes (Source: National Housing Federation housing supply analysis) reflecting decades of under-delivery relative to population growth and housing demand. While housing shortages are often discussed in political terms, the underlying causes are structural and deeply embedded in the institutional framework that governs land, planning and development.

Unlike many other sectors of the economy, housing supply cannot respond quickly to changes in demand. Residential development is influenced by a complex set of regulatory, financial and physical constraints that significantly limit the speed at which new housing can be delivered. As a result, increases in housing demand tend to translate more readily into rising prices and rents than into rapid increases in supply.

One of the most significant constraints arises from the planning system itself. The UK operates a discretionary planning system in which each development proposal must receive individual approval from local planning authorities. While the system is designed to balance development with environmental and community considerations, the process can be lengthy and uncertain. Planning decisions may take months or even years, and developers frequently face extensive negotiations regarding design, density, infrastructure contributions and environmental impacts.

Planning authorities also operate within a context of limited institutional capacity. Many local planning departments have experienced significant reductions in staffing over recent decades, resulting in fewer planning officers responsible for assessing increasingly complex development proposals. This capacity constraint can further slow the approval process and add uncertainty for developers and investors.

Environmental regulations, while essential for protecting natural ecosystems, can also influence development timelines and costs. Requirements related to biodiversity, water management, and environmental impact assessments can introduce additional layers of complexity to the planning process. In certain areas, development has been delayed by issues such as nutrient neutrality requirements or ecological considerations affecting protected habitats.

Another structural feature shaping the housing market is the Green Belt policy, which restricts development across large areas surrounding many major British cities. Originally introduced to prevent urban sprawl and preserve countryside landscapes, the Green Belt has

become a defining element of the spatial structure of UK cities. While it serves important environmental and planning objectives, the policy also limits the availability of land for new housing in locations where demand is often strongest.

Beyond regulatory considerations, the economics of land itself play a critical role in shaping housing supply. Land suitable for development in high-demand areas can command extremely high prices, reflecting both current planning permissions and expectations of future development potential. This dynamic can create significant barriers to entry for developers and increase the financial risks associated with residential projects.

The process of negotiating planning obligations further adds to development complexity. Local authorities frequently require developers to contribute to infrastructure, affordable housing provision or community facilities through mechanisms such as Section 106 agreements and the Community Infrastructure Levy (CIL). While these contributions play an important role in funding public infrastructure, they can also affect the financial viability of development projects and extend the negotiation process prior to construction.

Taken together, these structural features mean that housing supply in the UK responds only slowly to rising demand. When demand for housing increases (whether due to population growth, demographic change or economic factors) the result is often upward pressure on house prices and rents rather than a rapid expansion in new construction.

These constraints have profound implications for the evolution of the housing market. Persistent supply limitations contribute to rising house prices, which in turn make homeownership increasingly difficult for younger households to access. As the gap between incomes and house prices widens, a growing share of the population becomes reliant on the rental sector for long-term housing.

In this context, the expansion of Build-to-Rent developments can be seen as part of the market’s response to structural supply pressures. Institutional investors entering the residential sector are not simply responding to short-term market cycles; they are positioning themselves within a housing system where demand for professionally managed rental accommodation is likely to remain strong for the foreseeable future.

- The Erosion of the Traditional Homeownership Pathway

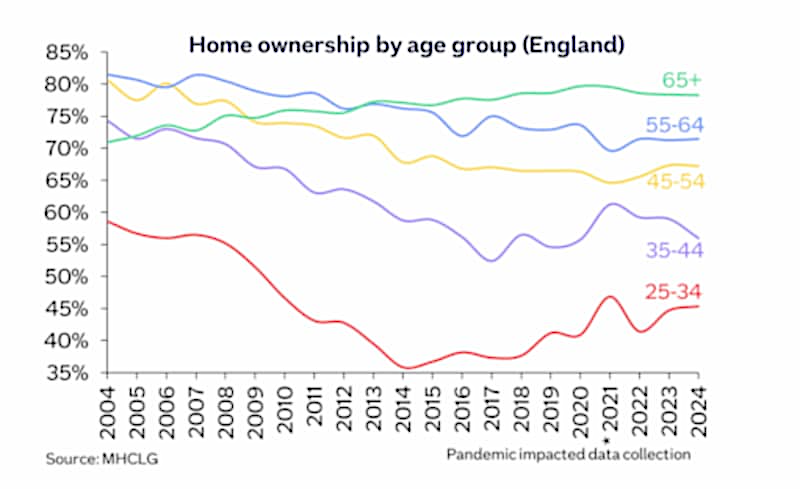

“Homeownership among households aged 25–34 fell from around 60–65% in the early 1990s to roughly 40% today, reflecting the increasing difficulty of accessing ownership.” Source: Institute for Fiscal Studies housing tenure analysis.

For much of the late twentieth century, homeownership was widely regarded as the natural destination of the British housing journey. Rising wages, accessible mortgage finance and relatively affordable housing allowed many households to transition from renting into ownership during early adulthood. Owning a home was not only a financial aspiration but also a central component of post-war social policy.

Over the past two decades, however, this pathway into ownership has become increasingly difficult to access for younger generations. House prices have risen substantially faster than average earnings, particularly in economically dynamic regions such as London and the South East. As a result, the ratio between house prices and household incomes has widened significantly, requiring many prospective buyers to accumulate deposits that are far larger than those faced by previous generations.

Mortgage regulation has also tightened following the global financial crisis of 2008. While these changes have strengthened financial stability within the banking system, they have also raised the barriers to entry for first-time buyers. Lenders now apply stricter affordability tests and often require higher deposits, particularly in markets where prices are elevated relative to income levels.

At the same time, broader changes in the labour market have altered the economic environment in which younger households make long-term housing decisions. Careers are increasingly characterised by greater mobility, shorter employment tenures and a growing presence of flexible or project-based work. These conditions can make the long-term financial commitment associated with homeownership less accessible or less attractive for some households.

Demographic shifts have further influenced housing patterns. An ageing population has led to longer periods of home occupation by older households, reducing turnover within the housing stock and limiting opportunities for younger buyers to enter the market. At the same time, population growth in major cities has intensified demand for housing in urban areas where supply constraints are most pronounced.

The combined effect of these trends has been the emergence of what is often described as “Generation Rent.” Today the private rented sector houses over 11 million people in England, representing roughly one in five households, illustrating the growing importance of rental accommodation within the UK housing system. Source: Office for National Statistics.

Increasing numbers of households now spend longer periods of their lives in rental accommodation, sometimes well into middle age. For many, renting is no longer a temporary stage preceding homeownership but a long-term housing arrangement.

This structural shift has important implications for the nature of the rental sector itself. Historically, the UK’s private rental market has been dominated by small individual landlords operating on a relatively fragmented basis. While this model has provided a large share of rental housing, it has also produced uneven standards of management, maintenance and tenant experience.

As renting becomes a long-term tenure rather than a transitional phase, expectations among tenants are beginning to evolve. Households who expect to rent for extended periods increasingly value stability, professional management and consistent service standards. These expectations mirror the qualities commonly associated with institutional real estate sectors such as student accommodation, hospitality or commercial property.

The emergence of Build-to-Rent developments can therefore be seen as a response to these changing dynamics within the housing market. Professionally managed rental communities offer a different proposition from traditional private renting, often incorporating on-site management, shared amenities and a greater emphasis on tenant experience. For institutional investors, this operational model also provides an opportunity to generate stable, long-term income streams from residential property.

In this sense, the development towards Build-to-Rent reflects not only financial innovation within real estate markets but also a broader transformation in the social and economic conditions shaping housing demand in the United Kingdom.

- The Institutionalisation of Rental Housing

“The UK Build-to-Rent sector has grown rapidly, with over 260,000 homes either completed, under construction or in planning across the country.” Source: British Property Federation BTR market reports

“Institutional investment in the UK Build-to-Rent sector has expanded rapidly over the past decade, with tens of billions of pounds of capital committed to rental housing development pipelines.” Source: Savills

Capital Flow Into BTR

Professionally

Managed Rental

Housing

Institutional Investment

Funds

- Pension Funds

BTR

Developers

- Insurance Companies

- Sovereign Wealth Funds

Alongside the structural changes reshaping housing demand, another powerful force has emerged within the residential market: the growing role of institutional capital. Over the past decade, residential property has increasingly attracted interest from pension funds, insurance companies and global investment managers seeking long-term, income-generating assets. This shift has played a central role in the development of the Build-to-Rent sector in the United Kingdom.

Historically, large institutional investors had relatively limited exposure to residential property in Britain. Unlike commercial real estate sectors such as offices, retail or logistics (where assets are typically held in large, professionally managed portfolios) the private rental market was highly fragmented. Individual landlords owning one or two properties dominated the sector, making it difficult for institutional investors to deploy capital at scale.

From the perspective of institutional capital, residential property offered several structural challenges. Rental housing involved managing large numbers of tenants, maintaining individual units and dealing with operational complexity that did not exist in other real estate asset classes. Without a professionally structured operating model, residential investment lacked the scalability and efficiency required by large investment funds.

The emergence of Build-to-Rent has begun to address these structural limitations. BTR developments are typically designed, financed and operated as integrated rental communities rather than individual units intended for sale. This approach allows residential property to be managed more like other institutional real estate sectors, with professional management teams overseeing leasing, maintenance and tenant services across entire buildings or portfolios.

For institutional investors, the appeal of such assets lies in the stability of residential rental income. Housing demand tends to be relatively resilient across economic cycles, as the need for accommodation remains constant regardless of broader economic conditions. This stability makes rental housing particularly attractive to long-term investors whose liabilities (such as pension payments or insurance obligations) extend over several decades.

Residential rental income also offers a degree of protection against inflation. Rental contracts are typically short in duration compared with commercial leases, allowing rents to adjust more frequently in response to changes in market conditions. In an environment of rising inflation, this ability to reprice income streams can be particularly valuable for investors seeking to preserve real returns.

Another factor contributing to the growing interest in residential real estate is the search for portfolio diversification. Traditional institutional real estate portfolios have long been concentrated in office, retail and industrial assets. However, structural changes in these sectors (such as the rise of e-commerce affecting retail or remote work reshaping office demand) have encouraged investors to diversify into alternative property sectors.

Within this context, residential rental housing has increasingly been viewed as a core component of diversified real estate portfolios. In markets such as the United States, professionally managed multifamily housing has long been established as a major institutional asset class. The UK Build-to-Rent sector can be understood in part as an evolution toward a similar model, adapted to the specific regulatory and planning environment of the British housing market.

The expansion of institutional investment into residential property has therefore not occurred in isolation. Rather, it reflects a broader trend toward the financialisation and professionalisation of housing, in which residential real estate becomes integrated into global capital markets. Build-to-Rent developments provide the operational structure through which this capital can be deployed effectively.

For developers, this shift has created new opportunities to partner with institutional investors in delivering large-scale rental housing projects. Such partnerships allow developers to focus on site acquisition, planning and construction while investors provide long-term capital and operational stability. The result is a development model capable of delivering housing at scale while aligning with the investment requirements of global capital markets.

The growing institutional presence within the residential sector is therefore likely to play a significant role in shaping the future structure of the UK housing market. As capital continues to flow into Build-to-Rent developments, the sector is gradually establishing itself as a distinct and increasingly important component of the country’s housing system.

- Planning Complexity and Barriers in Delivering Rental Housing

Development Process Timeline:

Land Acquisition > Planning Application > Planning Negotiation > Planning Permission > Financing > Construction > Completion >

While the structural demand for rental housing in the United Kingdom has strengthened considerably, translating this demand into new housing supply remains a complex and often protracted process. Residential development operates within a regulatory and economic framework that can significantly influence both the feasibility and the timing of projects. For Build-to-Rent developments in particular, the interaction between planning policy, development economics and investment requirements plays a central role in determining whether projects can proceed.

One of the defining characteristics of the UK development environment is the discretionary nature of the planning system. Unlike zoning systems where permitted land uses are predetermined, the British system requires individual development proposals to be assessed by local planning authorities on a case-by-case basis. While this approach allows flexibility in shaping urban environments, it also introduces a high degree of uncertainty for developers and investors.

Obtaining planning permission for a major residential scheme can involve lengthy negotiations concerning building height, density, design, environmental considerations and infrastructure provision. Local planning authorities must balance the need for new housing with community concerns, environmental protections and broader spatial planning objectives. As a result, the planning process for large residential developments can extend over several years before construction is able to begin.

Planning obligations further influence the economics of development. Through mechanisms such as Section 106 agreements and the Community Infrastructure Levy (CIL), developers are typically required to contribute toward local infrastructure, community facilities and affordable housing provision. These contributions are intended to ensure that new development supports the broader needs of local communities. However, they also form a significant component of development costs and are often subject to detailed negotiations between developers and planning authorities.

For Build-to-Rent projects, the structure of planning obligations can be particularly important. Traditional residential developments are frequently designed for the sale of individual units, allowing developers to recover capital through phased sales as construction progresses. In contrast, BTR developments are typically held as long-term investment assets, meaning that the economic viability of the scheme depends on the future rental income generated by the completed building. Planning requirements must therefore be considered carefully within the financial models used by investors and developers when assessing potential projects.

Environmental and regulatory considerations can also influence development timelines. Requirements related to biodiversity protection, environmental impact assessments, water management and energy performance have become increasingly prominent in the planning process. While these regulations are essential in promoting sustainable development, they can introduce additional complexity to project delivery and require specialised expertise during the design and approval stages.

Another factor shaping development feasibility is the availability and cost of suitable land. In many high-demand areas (particularly within major cities) the supply of development land is limited and highly competitive. Land values often reflect expectations regarding future planning permissions and development potential, meaning that acquisition costs can represent a substantial portion of overall project expenditure. Developers must therefore navigate a careful balance between land acquisition costs, construction expenses and anticipated rental income in order to achieve viable schemes.

Taken together, these factors highlight the intricate environment within which new housing must be delivered. The interaction between planning policy, land economics and investment requirements means that bringing a Build-to-Rent development from concept to completion involves navigating a series of regulatory and financial hurdles. Yet despite these complexities, the structural demand for rental housing and the growing interest from institutional capital continue to drive expansion within the sector.

Understanding these development dynamics is crucial for appreciating both the opportunities and the limitations associated with Build-to-Rent. While the sector holds considerable potential to contribute to housing supply, its growth will ultimately depend on the ability of developers, investors and policymakers to work within (and potentially refine) the institutional frameworks that govern the delivery of housing in the United Kingdom.

- The Future Role of Build-to-Rent in the UK Housing System

The emergence of Build-to-Rent represents more than the creation of a new niche within the residential property market. It signals a gradual reconfiguration of how housing is financed, delivered and managed within the United Kingdom. As the structural drivers examined earlier continue to shape the housing landscape, BTR is likely to become an increasingly important component of the country’s housing system.

One of the defining features of the sector is its ability to attract long-term institutional capital into residential development. Pension funds, insurance companies and global investment managers operate on investment horizons measured in decades rather than years. Their interest in rental housing reflects the search for stable income-generating assets capable of matching long-term financial liabilities. When combined with professional property management and operational scale, residential rental assets can offer income streams that resemble those found in other institutional real estate sectors.

This long-term investment perspective also has implications for the nature of housing delivery. Traditional residential development in the United Kingdom has largely been oriented toward individual unit sales. In contrast, Build-to-Rent developments are designed as long-term operational assets, encouraging a different approach to building design, property management and tenant experience. Features such as shared amenities, on-site management teams and community-focused spaces are often incorporated to enhance tenant satisfaction and reduce turnover, thereby supporting stable rental income.

The sector is also beginning to evolve geographically. Early BTR developments were concentrated primarily in major metropolitan areas where rental demand was strongest and institutional capital could be deployed at scale. However, as the sector matures, developments are increasingly appearing in regional cities and suburban locations. Improvements in transport infrastructure, changing working patterns and demographic shifts are expanding the range of locations where professionally managed rental housing can operate successfully.

Partnerships between developers, institutional investors and housing associations may also play a growing role in shaping the future of the sector. Housing associations possess extensive experience in managing residential assets and delivering large-scale housing developments, while institutional investors bring access to substantial pools of capital. Collaborative models that combine these capabilities have the potential to support the delivery of mixed-tenure developments that integrate both market-rate and affordable housing.

At the same time, the growth of institutional rental housing is likely to attract increased public and political scrutiny. Housing occupies a unique position within society, serving not only as a financial asset but also as a fundamental social need. As a result, the expansion of Build-to-Rent developments will inevitably be accompanied by ongoing debates concerning affordability, tenant protections and the broader role of institutional investors within the housing market.

Nevertheless, the structural forces underpinning the sector’s growth remain significant. Persistent housing supply constraints, demographic pressures and evolving labour market conditions suggest that demand for professionally managed rental accommodation will remain strong for the foreseeable future. In this environment, Build-to-Rent developments offer a mechanism through which large-scale investment can be directed toward the delivery of new housing.

Rather than replacing existing housing tenures, BTR is likely to become one of several complementary components within a diversified housing system. Alongside owner-occupation, social housing and traditional private renting, institutional rental housing has the potential to form an additional pillar supporting housing provision in the United Kingdom.

- Conclusion

The growth of Build-to-Rent should not be understood simply as a response to short-term market conditions. Instead, it reflects a convergence of deeper structural forces shaping the British housing landscape. Persistent constraints on housing supply, the increasing difficulty of accessing homeownership and the growing presence of institutional capital within real estate markets have collectively created the conditions for the emergence of a professionally managed rental sector.

Historically, Britain’s housing system has evolved through several distinct phases. The early twentieth century was characterised by widespread renting, followed by the expansion of state-led housing provision in the post-war period. From the late twentieth century onwards, homeownership became the dominant tenure, supported by political and financial systems that encouraged property ownership. Today, however, the housing system is entering a new stage in which rental housing is once again becoming a central component of urban living.

In this evolving landscape, Build-to-Rent developments represent a bridge between housing need and institutional capital. By combining professional management with long-term investment structures, the sector offers a model capable of delivering rental housing at scale while aligning with the requirements of global investors.

The continued growth of the sector will depend on the interaction between developers, investors and policymakers. Planning frameworks, development economics and regulatory structures will all influence the pace at which new rental housing can be delivered. Yet the underlying forces driving the sector’s expansion suggest that Build-to-Rent will remain an increasingly important feature of the UK housing market in the years ahead.

As the housing system continues to evolve, the institutionalisation of rental housing may prove to be one of the most significant developments in British residential real estate for generations.

In this sense, the emergence of Build-to-Rent may represent not merely a new housing product, but the institutionalisation of residential real estate within the United Kingdom.

THE END

The cantilevered and stepped massing plays into the building’s sustainability benefits, as it forms balconies and green roofs that allow occupants fresh air and stunning views of the city.

Comments are closed.